Hedge Funds Versus Hedged Mutual Funds: An Examination of Long/Short Funds; A Performance Update

David F. McCarthy

D.F. McCarthy LLC

dfm@dfmccarthy.com

and

Brian M. Wong

SUMMARY AND KEY FINDINGS

April 5, 2019

Introduction

After a period of initial asset growth, more questions are being asked of the liquid alternative mutual fund marketplace. See, for example: “Liquid Alternatives Haven’t Lived Up to the Hype (Yet).” Morningstar Blog (August 2, 2018), and “Liquid Alternatives: Alternative Enough?” CFA Institute, (September 24, 2018).

To better understand how a segment of this market is performing, and developing over time, this paper updates an earlier work, “Hedge Funds Versus Hedged Mutual Funds: An Examination of Long/Short Funds” (The Journal of Alternative Investments, Winter 2014; referred to herein as McCarthy (2014)). In this updated analysis, performance of the equity long/short mutual funds examined in McCarthy (2014) is presented for the period July 1, 2013, through December 31, 2018. As in the earlier paper, the performance of these equity long/short mutual funds is compared to the S&P 500 Index and traditional hedge fund indexes, and are segmented into funds sponsored by diversified investment firms versus specialized investment firms. Included are analyses of comparative correlations and betas, absolute and risk-adjusted returns, performance persistence, survivorship rates, the substantial change in individual fund size, and the effect of performance on asset flows.

Below is a summary of the key findings of this analysis. The full paper can be found on SSRN at https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3367511 .

Key Findings:

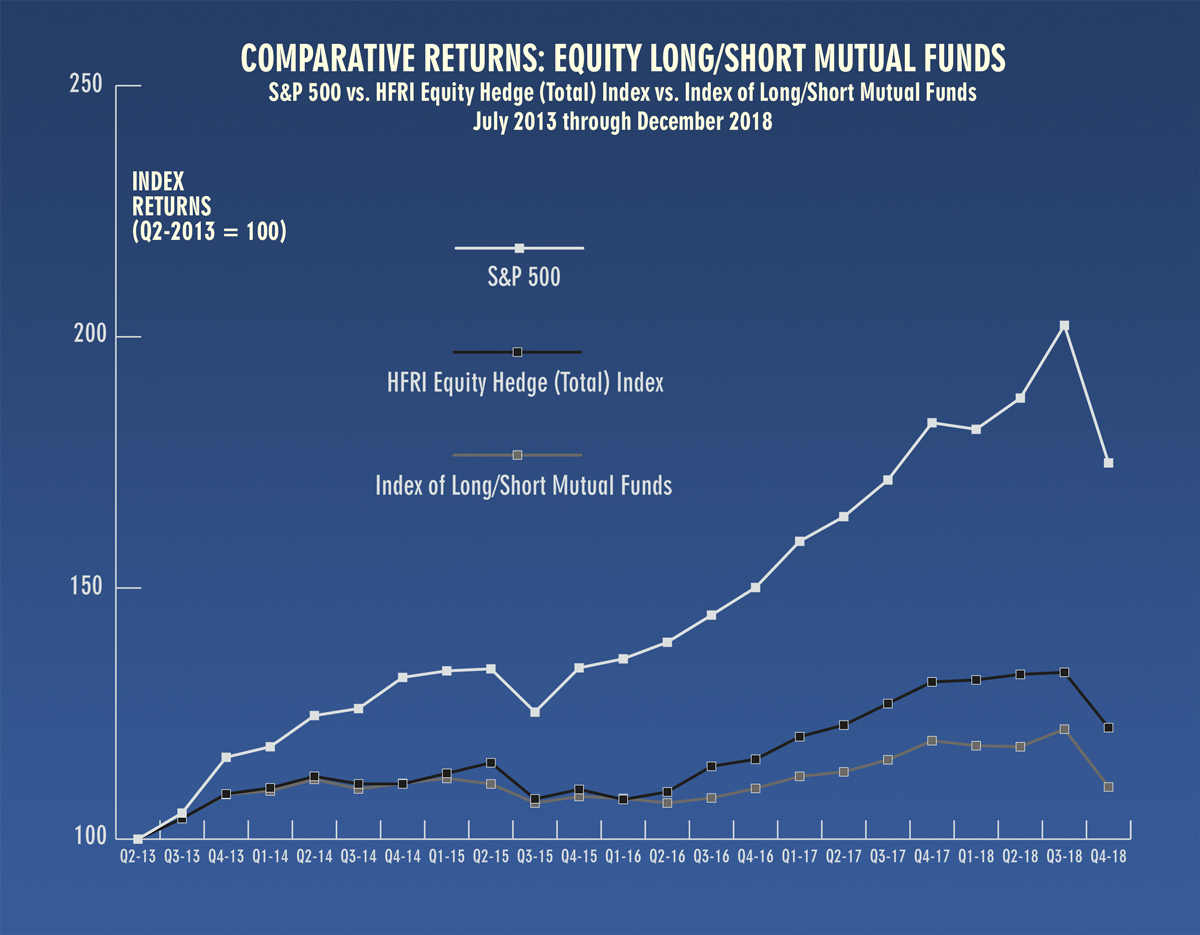

Key Finding #1: Equity long/short mutual funds substantially underperformed the S&P 500 Index over the period July 2013 - December 2018.

This underperformance was markedly the case in absolute return terms (10.7% p.a. for the S&P 500 versus 1.8% p.a. for the index of equity long short mutual funds). Further, the index of long/short mutual funds had poor risk adjusted performance (alpha) as well. As a group, equity long/short mutual funds generated -3.8% p.a. alpha over this period, with no single mutual fund generating a positive alpha. The graph below illustrates the comparative cumulative performance over this period of the S&P 500 Index, the HFRI Equity Hedge (Total) Index, and the Index of Equity Long/Short Mutual Funds developed for this paper.

Key Finding #2: Equity long/short mutual funds continued to exhibit a similar correlation and beta to the S&P 500 as equity hedge fund indexes.

As in McCarthy (2014), the Index of Equity Long/Short Mutual Funds demonstrated a similar correlation, standard deviation, and beta to the S&P 500 over the 6/2013 - 12/2018 period as leading equity hedge fund indexes. These results indicate that equity long/short mutual funds continue to employ strategies and leverage similar to that found in traditional hedge funds.

Key Finding #3: Equity long/short mutual funds underperformed both the HFRI Equity Hedge (Total) Index and the DJ-CS L/S Equity Hedge Fund Index from July 2013 - December 2018.

Despite having slightly higher beta to the S&P 500 over this bull market period, the Index of Equity Long/Short Mutual Funds underperformed both the HFRI Equity Hedge (Total) Index and the DJ-CS L/S Equity Hedge Fund Index from July 2013 - December 2018 (1.8% p.a. vs. 3.7% p.a. and 4.2% p.a. respectively). While these differences are not statistically significant, they do differ from the earlier time period in McCarthy (2014) when returns were approximately equal across the three groups.

Key Finding #4: Equity long/short mutual funds sponsored by diversified investment firms continued to outperform those sponsored by specialized investment firms.

As was the case in McCarthy (2014), the equity long/short mutual funds sponsored by diversified investment firms held an approximately 200BP per annum performance advantage over those sponsored by specialized investment firms for the period 7/2013 - 12/2018. Approximately half of the difference in this later time period may be explained by the higher beta of those funds sponsored by diversified investment firms.

Key Finding #5: There is no evidence of positive performance persistence among equity long/short mutual funds.

Top performing equity long/short mutual funds (i.e. in the top half of comparable funds) in one year showed a roughly equal chance of being in the top half or bottom half in the subsequent year. Bottom half performers in one year were also approximately equally likely to be in the top or bottom half, but with a higher likelihood of being shut down in the subsequent year.

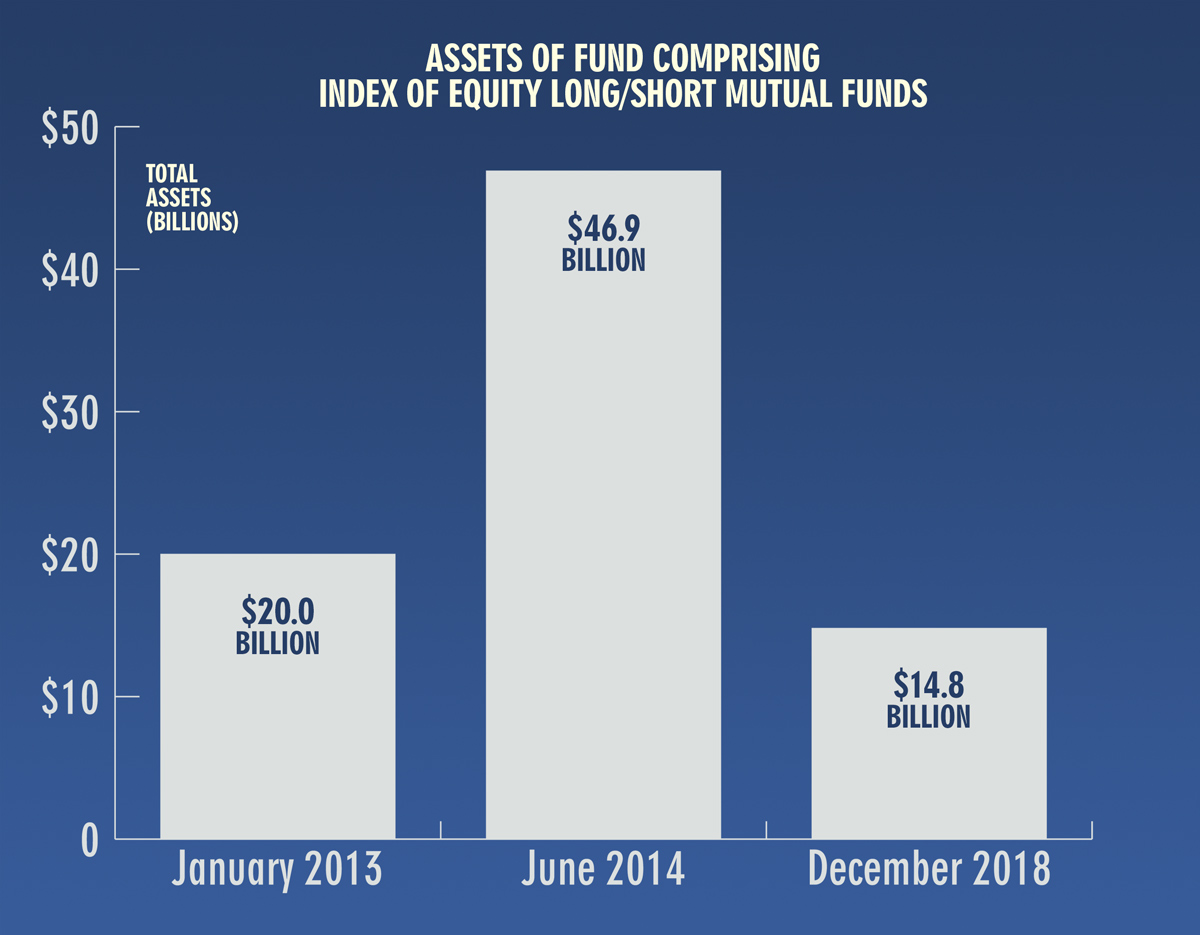

Key Finding #6: The equity long/short mutual funds in this analysis experienced a period of rapid AUM growth from 2013 to 2014, with an equivalent outflow by the end of 2018.

The average size of an equity long/short mutual fund in December 2018 was approximately the same as in January 2013. However, that masks the very substantial change in assets (up and down) over that period as the table below shows.

Assets managed by the funds in this analysis more than doubled from January 2013 to June 2014. That increase was then more than completely reversed by December 2018. Additionally, the five largest funds as of January 2013 held $13.7B in assets. By December 2018, assets in these five funds had declined to $4.5B (a 67% decline), with only one of them still among the five largest. This decline was almost exactly matched by the $8.7B increase in assets from 2013 to 2018 experienced by the five largest funds as of December 2018.

Key Finding #7: The fund closure rate of equity long/short mutual funds was similar to that of long only equity mutual funds.

Of the 47 funds in this category as of January 2013 (see McCarthy (2014)), 17 closed before December 2018, and another 4 substantially changed investment strategy. This rate of closure was found to be similar to that of general US equity mutual funds over this time period.

ENDNOTE:

Please see the complete paper for a fuller explanation of the analyses, results, and conclusions. It can be found on SSRN at:

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3367511.